Truly digital is all about transformation spanning experience, engagement and business engine layers. Focusing only on enabling new channels or touch points is not enough. There are a set of basic characteristics that a Core banking solution must demonstrate to enable banks to achieve the intended results:

- Creating compelling customer experience

- Exploiting the power of core operations and

- Reinventing business models

This article describes some of the most critical basic characteristics across three dimensions for core transformation.

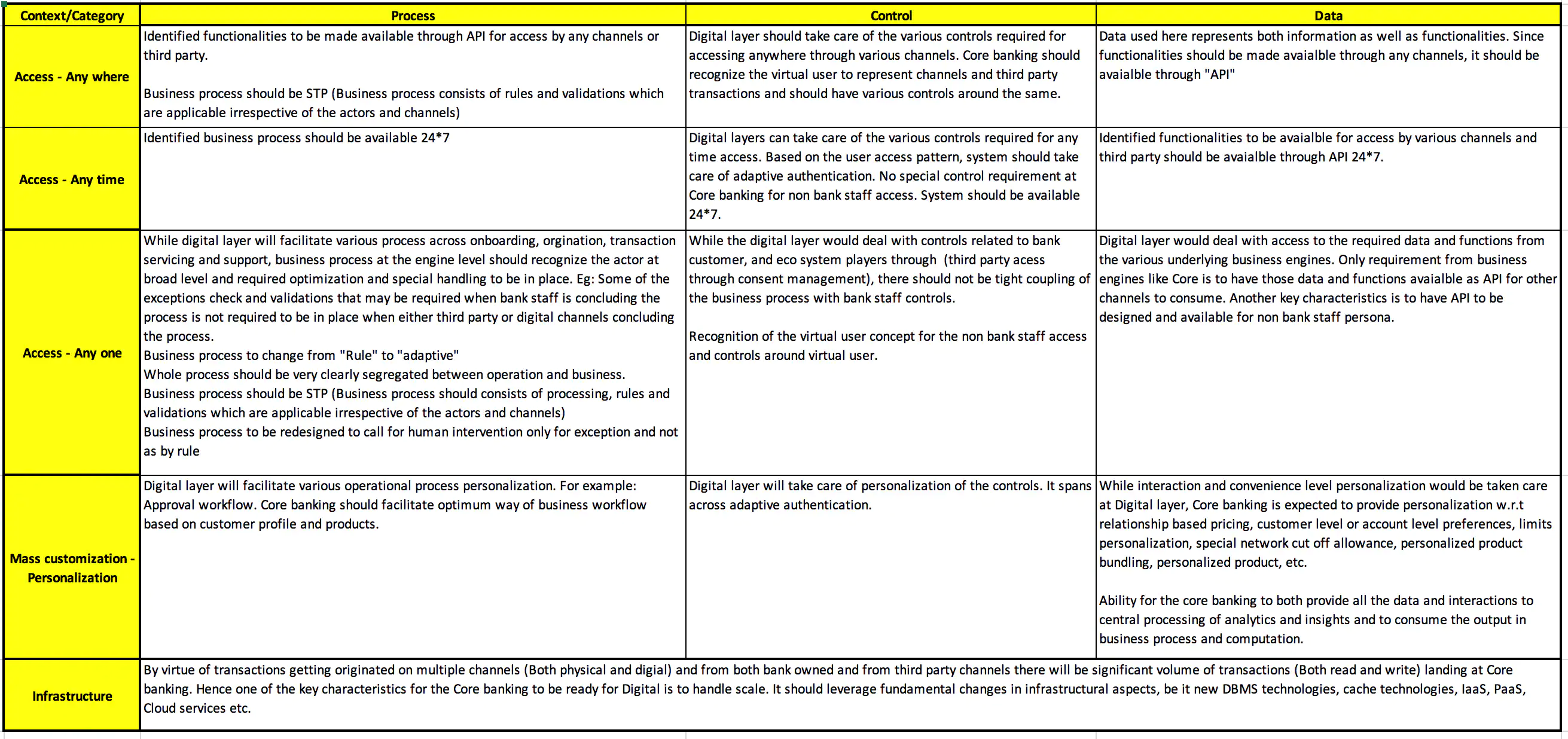

Before getting into the details, let us look at the change of context w.r.t

- Accessing banking services – (A)

- Infrastructure – (I)

- Mass production to mass customization – (M)

In short, it can be referred to as “A.I.M”. (Access, Infrastructure and Mass customization)

Accessing Banking Services

In the first phase of automation banking services were accessed

- At designated places like Branches

- At designated time like branch operation time and

- By designated people like bank staff (Teller, RM, Agent..)

In the next phase, which can be referred to as the “Access” phase, banking services were made available as

- Anywhere through various digital channels

- Any time through various Digital channels at user convenience

- Any one – Not only bank staff but also various bank customer persona like Retail and Corporate and third party through open banking. Literally “access” was provided to any one and of course with required controls and consent

| Phase | Where | When | Who | ||||

|---|---|---|---|---|---|---|---|

| Automation | Designated Places | Designated Time | Designated People | ||||

| Access | Any where | Any time | Any one |

Hence there is a fundamental shift of context from “Designated*” to “Any*”. This clearly carves out the path for the digital engagement layer to take care of personalized data, control and engagement and at the same time clearly emphasizes the significance of core banking.

Infrastructure

There is a considerable change in infrastructural aspects for computing power, storage, network, monitoring, IaaS, PaaS etc. Considering that transaction volumes are growing exponentially (both read and write), solutions like Core banking should leverage such infrastructures.

Mass Customization

Due to various factors and predominantly change in customer expectation, there is a shift from mass production to mass customization. From the bank’s perspective, this can also be referred to as “What I have” to “What you need”. It is a well-known fact that personalization is the key to achieving mass customization. Let’s have a look at how it plays out:

- Interaction: Favorites menus, frequently and recently used, themes, profile photo, etc.

- Content: inbox, date format, amount format, language preference etc.

- Convenience: Personalized reports, query template, favorite accounts, primary account etc.

- Functionality and control: Payment template, personalized limits, VAM etc.

- Product level: Personalized product offer based on real KYC, tailoring of the product, etc.

While personalization for interaction, convenience, control can be dealt with at the digital engagement layer, product, services and functionality-level personalization should be dealt with at the business engine level as well.

Based on these changing paradigms, business engines like core banking should have some critical attributes that are mapped below to the three dimensions of (A.I.M):

Conclusion

To realize the benefits of digital transformation, digitization is required across experience, engagement and business engine layers. For supporting digitization of core, it should exhibit a set of characteristics across three dimensions (A.I.M). To mention a few:

- APIs for required functions

- Rules for adaptive business process

- Business processes demanding human intervention only on exception

- Ability to consume relationship-based pricing

- 24*7 availability

- Ability to deal with volumes

- Core business process to be independent of actors and channels. Any specific handling required for actors to be dealt with separately

- Leverage various infrastructural aspects like new DBMS technologies, cache technologies, cloud services etc.

Is your core banking ready for Digital age? Does it exhibit these characteristics? Do share your views in the comments section below.

Investec Selects Infosys Finacle SaaS Platform on Microsoft Azure for Digital Banking Transformation

Let’s Discuss

Fill out the form below and we will get back to you shortly. Alternately, you can also contact our regional offices